RBI Maintains Status Quo; Announces Measures to Support Capital Flows & Rupee Stability

#

5th Jun, 2026

- 1061 Views

NDNC disclaimer: I hereby authorize Bajaj Life Insurance Limited. to call me on the contact number made available by me on the website with a specific request to call back. I further declare that, irrespective of my contact number being registered on National Customer Preference Register (NCPR) or on National Do Not Call Registry (NDNC), any call made, SMS or WhatsApp sent in response to my request shall not be construed as an Unsolicited Commercial Communication even though the content of the call may be for the purposes of explaining various insurance products and services or solicitation and procurement of insurance business

Mr. Srinivas Rao Ravuri, Chief Investment Officer, Bajaj Life

Policy Decision: RBI Keeps Rates Unchanged, Retains Neutral Stance

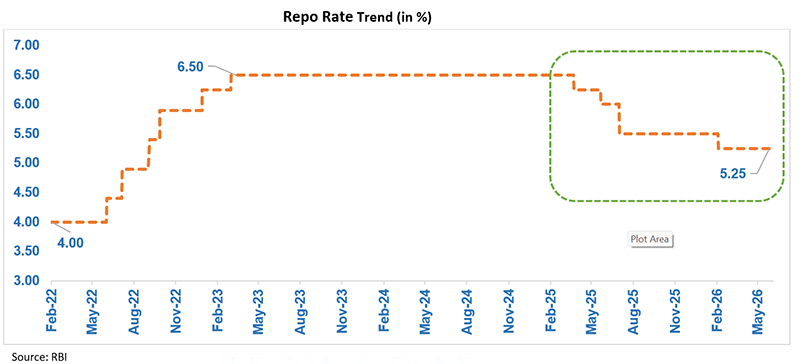

The Reserve Bank of India’s Monetary Policy Committee (MPC) unanimously kept the policy repo rate unchanged at 5.25% and maintained its neutral stance. The decision reflects RBI’s preference to preserve policy flexibility amid heightened geopolitical tensions, elevated energy prices, supply chain disruptions and growing uncertainty over the global growth-inflation outlook. The central bank believes that it is prudent to wait for greater clarity before altering its policy stance.

Growth: Domestic Environment Resilient, Global Headwinds Intensify

India’s economy continues to demonstrate resilience despite a challenging global backdrop. Real GDP growth for FY2025-26 is estimated at 7.6%, supported by strong private consumption and fixed investment. High-frequency indicators such as GST collections, E-way bills, PMI readings, vehicle sales and infrastructure activity continue to indicate healthy economic momentum.

However, the RBI has lowered its FY2026-27 growth projection to 6.6% from 6.9% projected in April. Quarterly growth is now expected at 6.6% in Q1, 6.3% in Q2, 6.5% in Q3 and 6.8% in Q4. The downgrade reflects concerns around higher energy prices, supply-chain disruptions, elevated logistics costs and the risk of a below-normal monsoon.

Going ahead, the rise in prices of energy and other inputs, coupled with supply disruptions, is likely to weigh on economic activity. The full impact, however, will depend on the duration of the conflict and time taken for normalization of supply chains. Government support measures, robust capital expenditure, healthy credit growth and resilient services exports are expected to cushion some of these external shocks.

Inflation: Rising Energy Prices Push Inflation Outlook Higher

Headline CPI inflation remained below the RBI’s target during March and April at 3.4% and 3.5%, respectively. Core inflation remained stable at around 3.7%, indicating that underlying demand-side price pressures remain contained.

Nevertheless, the inflation outlook has deteriorated due to sustained high crude oil prices, rising input costs and weather-related risks. The Indian crude basket averaged around US$110 per barrel during April-May 2026, while fuel price pass-through has started becoming visible in domestic markets.

Accordingly, RBI has raised its FY2026-27 inflation forecast to 5.1% from 4.6% projected in April. Quarterly inflation is projected to be at 4.2% in Q1, 5.1% in Q2, 5.9% in Q3 and 5.4% in Q4. The outlook remains vulnerable to further commodity price shocks, supply-chain disruptions, monsoon uncertainties and potential El Niño conditions.

External Sector: Measures Announced to Attract Capital and Support the Rupee

India’s external sector has navigated the challenges of elevated tariffs in FY 2025-26; however, recent geopolitical situation has resulted in higher energy price and increase pressure on currency. Foreign exchange reserves remain healthy at US$682.3 billion, providing nearly 11 months of import cover however they are down from the peak of $728 in Feb 2026.

However, the surge in energy prices and persistent trade policy uncertainties continue to pose upside risks to India’s current account deficit in FY 2026-27. The foreign portfolio investors (FPIs) have also remained cautious, with net outflows of US$13.7 billion so far in FY2026-27, primarily from equities. This resulted in a significant depreciation of exchange rate, which hit a record low of close to 97 INR per USD in May 2026.

To address this, RBI announced several measures during this policy which are aimed at attracting foreign capital and strengthening our balance of payments:

• Expansion of the Fully Accessible Route (FAR) by including all new issuances of 15-year, 30-year and 40-year government securities.

• Removal of certain investment restrictions for FPIs in government securities.

• Increase in investment limits for NRIs, OCIs and other Persons Resident Outside India (PROIs) in listed equities.

• Concessional forex swap facility for ECB borrowings by PSUs until September 2026.

• Full hedging-cost support for banks raising fresh FCNR(B) deposits.

• Restoration of the export proceeds realization period to nine months.

These measures, along with tax incentives announced by the Government for foreign investors, are intended to improve capital inflows, support government borrowing requirements and strengthen the rupee amid global volatility.

Liquidity & Financial Conditions: RBI Continues Proactive Liquidity Management

System liquidity remained comfortable with an average surplus of ₹2.63 lakh crore since the April policy. The RBI conducted a US$5 billion long-term forex swap auction along with variable rate repo operations to ensure adequate liquidity.

Short-term money market rates moderated initially before facing some pressure in May. The 10-year G-Sec yield softened following the West Asia ceasefire announcement but later firmed up due to renewed inflation concerns. Credit growth remains robust, with overall credit from all sources growing 15.4%, while bank credit expanded by 16.2% year-on-year. The RBI reiterated its commitment to ensuring adequate liquidity and facilitating smooth monetary transmission.

Financial Stability: Systemic Health Remains Healthy

India’s financial system continues to remain healthy, supported by strong capital buffers, improving asset quality and adequate liquidity. Scheduled commercial banks reported a CRAR of 17.68%, while gross NPAs declined further to 1.73% in Mar 2026 from 2.22% in Mar 2025. Liquidity coverage ratio stood at 123.7%.

NBFCs also maintained strong capital positions, with total CRAR at 24.7% and showed continued improvement in asset quality with gross NPAs falling to 1.83% in Mar 26 from 2.25% in Mar 2025.

Outlook: Growth Moderates, Inflation Rises; RBI Focus Shifts to External

Resilience

The June policy reflects a more cautious assessment of the economy. While domestic economic activity remains resilient, the prolonged West Asia conflict, elevated crude oil prices, supply-chain disruptions and weather-related risks have led to a downgrade in growth projections and an upward revision in inflation forecasts.

Importantly, the RBI has maintained status quo on policy stance with a series of measures aimed at attracting foreign capital, improving balance-of-payments stability and containing excessive volatility in the rupee. The strong emphasis on maintaining orderly foreign exchange markets suggests that external sector stability has become a key policy priority at the current juncture.

If energy prices remain elevated and inflationary pressures become broad-based, the RBI may come under pressure to raise interest rates in FY27. However, the fixed income market has already priced in the possibility of a rate hike, as reflected in the current elevated yield levels. Consequently, we expect the 10-year G-Sec yield to trade in the 6.90%–7.20% range, while high-quality corporate bonds in the 3–5 year segment continue to offer attractive risk-adjusted return opportunities. The trajectory of crude oil prices, monsoon developments, capital flows and geopolitical conditions will remain key variables to watch over the coming quarters.

Annexure:

Repo Rate – The interest rate at which the RBI lends money to commercial banks.

CRR – The share of a bank’s total deposits that must be kept with the RBI in cash.

Stance – It gives an indication to the future policy action.

SDF – The rate at which Banks lend to RBI without collateral.

MSF –The rate at which RBI lends (provides emergency liquidity) to Banks.

Enter your email address to subscribe to this blog and receive notifications of new posts by email.

Facebook

Twitter

pintrest

instagram

Whatsapp

Linkedin

More