RBI Holds Rates Steady Amid Rising Global Uncertainty; Maintains Neutral Stance

#

8th Apr, 2026

- 1263 Views

NDNC disclaimer: I hereby authorize Bajaj Life Insurance Limited. to call me on the contact number made available by me on the website with a specific request to call back. I further declare that, irrespective of my contact number being registered on National Customer Preference Register (NCPR) or on National Do Not Call Registry (NDNC), any call made, SMS or WhatsApp sent in response to my request shall not be construed as an Unsolicited Commercial Communication even though the content of the call may be for the purposes of explaining various insurance products and services or solicitation and procurement of insurance business

Mr. Srinivas Rao Ravuri, Chief Investment Officer, Bajaj Life

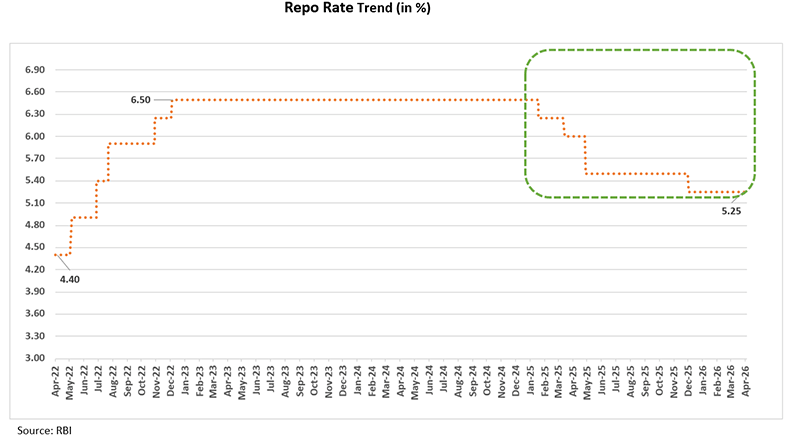

Policy Decision: RBI Maintains Status Quo with Neutral Stance

The Reserve Bank of India’s Monetary Policy Committee (MPC) kept the policy repo rate unchanged at 5.25% and continued with its neutral stance. The decision reflects a balanced approach considering rising global uncertainties, particularly due to escalating geopolitical tensions and disruptions in global supply chains. While domestic fundamentals remain strong, the RBI has chosen to stay vigilant and wait for further clarity on evolving macroeconomic conditions.

Growth Outlook: Strong Fundamentals, But External Risks Emerging

The outlook for FY2026–27 has been slightly moderated, with GDP growth projected at 6.8% in Q1 (vs 6.9% earlier), 6.7% in Q2 (vs 7.0%), 7.0% in Q3, and 7.2% in Q4, resulting in a full-year growth estimate of 6.9%, reflecting the potential impact of higher energy prices, supply chain disruptions, and global uncertainty arising from the ongoing West Asia conflict. Despite these headwinds, domestic demand, government infrastructure spending, and continued strength in services are expected to provide stability to growth.

India’s economic growth remains resilient, supported by robust consumption, sustained investment activity, and healthy balance sheets of corporates and financial institutions. GDP growth for FY2025–26 is estimated at 7.6%, indicating strong underlying momentum.

Inflation: Currently Benign, But Risks Tilted Upwards

Inflation remains under control, with recent readings staying below the RBI’s target. Core inflation pressures are also muted, indicating limited underlying price stress.

The inflation outlook faces upside risks, primarily due to higher global energy prices, potential supply disruptions, and weather-related uncertainties such as the possibility of El Niño. The RBI has projected inflation at 4.6% for FY2026–27, suggesting that while current levels are comfortable, future risks need close monitoring.

External Sector: Stable but Vulnerable to Global Developments

India’s external position remains stable, supported by strong services exports and steady remittance flows. However, the trade deficit has widened due to higher imports, especially driven by rising commodity prices.

Global uncertainties, including slower trade growth and volatile financial markets, pose risks to the external sector. Nevertheless, strong foreign exchange reserves provide a buffer against external shocks.

Liquidity & Financial Conditions: RBI Remains Proactive

Liquidity conditions in the banking system continue to remain comfortable. The RBI has actively undertaken measures such as open market operations and forex interventions to ensure adequate liquidity and smooth transmission of policy rates.

Interest rates across money markets have remained relatively stable, although some upward pressure has been observed due to global factors and rising yields. The RBI reiterated its commitment to proactive liquidity management going forward.

Financial Stability: Banking System Remains Strong

India’s financial system continues to demonstrate strength, with banks and NBFCs maintaining robust capital adequacy, improving asset quality, and stable profitability. Credit growth remains strong and broad-based, indicating healthy demand across sectors.

Outlook: Wait-and-Watch Approach Amid Elevated Uncertainty

The RBI’s policy reflects a balanced and cautious stance. While domestic economic fundamentals remain strong, rising geopolitical tensions and global uncertainties have increased risks to both growth and inflation.

The central bank appears to be in a wait-and-watch mode, prioritizing stability while retaining flexibility to act as conditions evolve.

From a market perspective:

• Equity markets may remain volatile in the near term due to global developments.

• Bond yields could remain elevated given inflation risks and global rate movements.

• Policy direction is likely to remain stable unless there is a significant shift in inflation or growth dynamics.

Overall, the current policy suggests that the RBI is focused on balancing growth and inflation while navigating external uncertainties, and any future action will be data-dependent and guided by evolving global and domestic conditions.

We expect the 10‑year G‑Sec yield to trade in the 6.80%–7.10% range and continue to prefer 3-Year corporate & 30-50 Year G-Sec bonds, given attractive yield.

Annexure:

Repo Rate – The interest rate at which the RBI lends money to commercial banks.

CRR – The share of a bank’s total deposits that must be kept with the RBI in cash.

Stance – It gives an indication to the future policy action.

SDF – The rate at which Banks lend to RBI without collateral.

MSF –The rate at which RBI lends (provides emergency liquidity) to Banks.

Enter your email address to subscribe to this blog and receive notifications of new posts by email.

Facebook

Twitter

pintrest

instagram

Whatsapp

Linkedin

More